It's been a tough year for investors in the Gold Miners Index (GDX), with the ETF sliding more than 10% year-to-date and massively underperforming the S&P-500 (SPY). The most frustrating thing about this underperformance is that it's despite inflation readings that have hit new multi-decade highs and negative real rates that are sitting near multi-decade lows. The good news is that this massive divergence between where gold (GLD) should be trading and the fundamental backdrop has led to a significant decline in gold miners, leaving them at their most attractive valuations since March 2020. In this update, we'll look at three that look like solid buy-the-dip candidates:

(Source: TC2000.com)

Barrick Gold (GOLD), Hecla Mining (HL), and Eldorado Gold (EGO) have little in common, with one being the world's 2nd largest gold producer, another being a ~500,000-ounce gold producer, and the third being the only primary silver miner focused on solely Tier-1 jurisdictions. However, the three do share one common trait: they're all sitting near oversold levels heading into 2022. In Barrick's case, the stock is trying to find support at a multi-year trend line, while both Hecla and Eldorado Gold are trading in the lower portion of their trading ranges after giving up significant ground over the past year. Let's take a closer look below:

Beginning with Barrick Gold, the company has had a very difficult year, with a mechanical mill failure at its Goldstrike roaster in Nevada, having to lap production from Porgera with the asset offline this year, and dealing with inflationary pressures. However, despite the difficult backdrop, the company has managed to keep its costs near $1,000/oz, which is in line with its initial guidance. This translates to 40% plus margins based on an average realized gold price of $1,800/oz, a very respectable figure.

During Barrick's most recent quarter, the company reported revenue of $2.83BB, a 20% decline due to lower production and a much lower average realized gold price. Not surprisingly, this led to continued selling pressure in the stock. However, the company was up against difficult year-over-year comps due to a record gold price in Q3 2020, and I would argue that this weak quarter was already priced into the stock, with GOLD down 40% from its Q3 2020 highs.

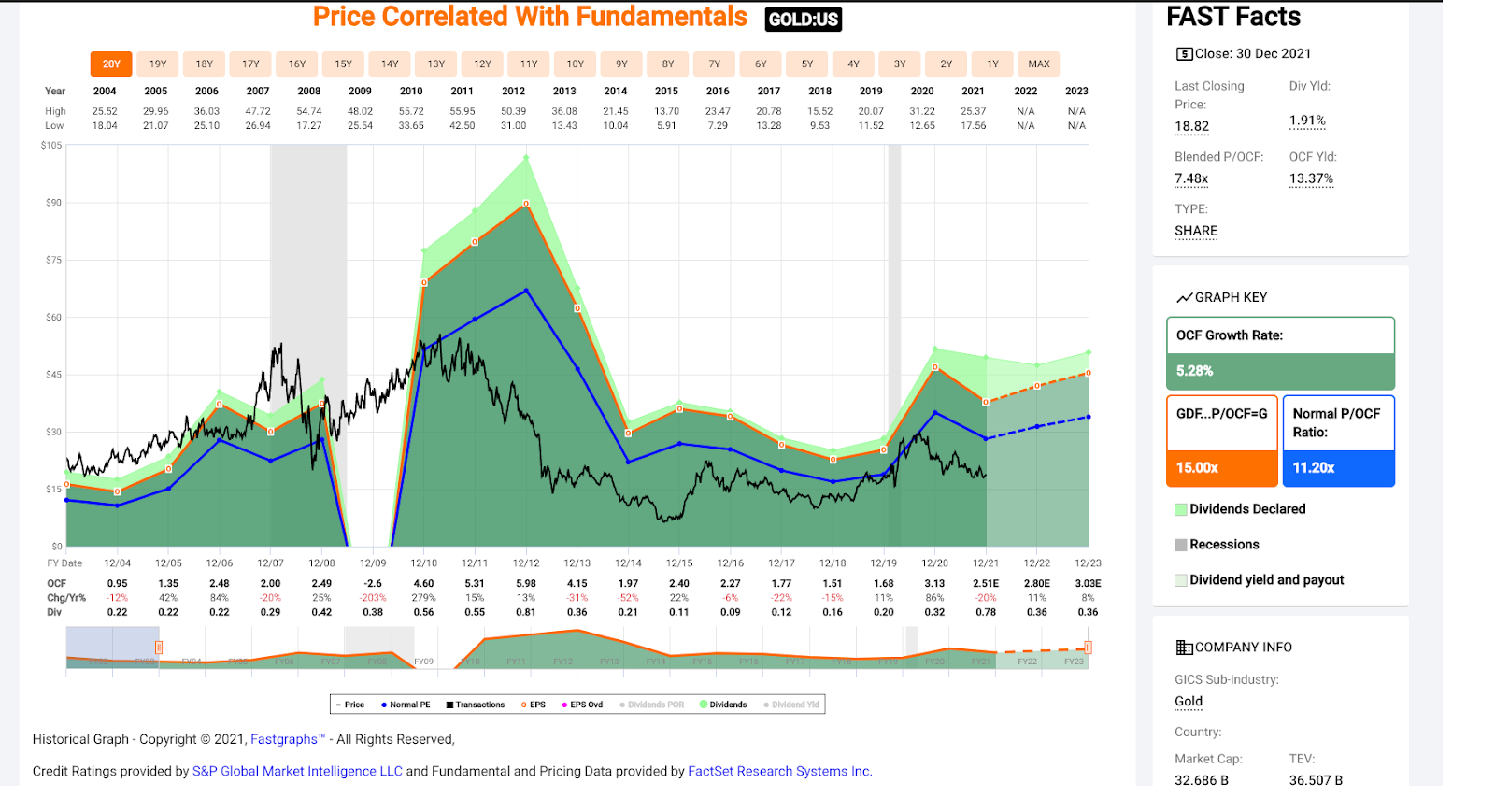

(Source: FASTGraphs.com)

As shown in the chart above, Barrick has historically traded at a cash flow multiple of 11, yet it currently trades at ~7x cash flow based on conservative FY2022 estimates of $2.70. This is a dirt-cheap valuation for the world's 2nd largest gold producer, especially considering that it also has a meaningful copper component, which should justify a small premium relative to historical levels given the attractive supply/demand picture for copper. This is related to the surge in electric vehicle demand that we have seen and will continue to see throughout the decade.

Based on what I believe to be a fair cash flow multiple of 10, I see a fair value for Barrick of $27.00, translating to nearly 50% upside from current levels. Notably, the stock is also pulling back to a major support zone and finding support here, pointing to this being a favorable area on the chart to accumulate the stock. So, if we see any weakness below $18.50, I would view this as a low-risk buying opportunity.

(Source: TC2000.com)

The second name worth keeping an eye on is Eldorado Gold, an intermediate gold producer with operations in Canada and Turkey. EGO was one of the only gold producers to raise its production guidance this year despite COVID-19 related headwinds, which affected productivity sector-wide, now expecting to produce 470,000 ounces of gold. If we look ahead to FY2023 and FY2024, production will increase further to ~505,000 ounces of gold, albeit at costs slightly above the industry average ($1,100/oz).

However, the major story for EGO is its Skouries Project in Greece, where the company recently completed a Feasibility Study. This advanced project where construction began in 2016 already has some infrastructure in place, but construction was halted, given that EGO didn't clear support from the Greek Government. However, with a new Conservative government in place, EGO is looking at restarting construction, hoping to begin production at Skouries by 2025. Based on the recent study, Skouries can produce 300,000 plus gold-equivalent ounces per annum at negative costs after including by-product credits from copper.

(Source: Company Presentation)

If we look at the chart above, we can see that this would dramatically affect EGO's production profile, increasing gold production to nearly 700,000 ounces per annum, or a nearly 70% increase from FY2021 levels. Meanwhile, given the extremely low costs, it would make EGO a low-cost producer vs. a high-cost producer currently. This should translate to a re-rating in the stock if Skouries gets the green light, given that higher-margin producers often trade at a premium to their peers.

(Source: TC2000.com)

Looking at EGO's technical picture, the stock looks to be trying to build the right side of a new base and looks to be under accumulation. So, with the stock trading at less than 0.75x book value and with the technical picture improving, I would view any pullbacks below $8.80 as low-risk buying opportunities. Assuming Skouries performs as planned and can be built with minimal share dilution, I see a fair value for EGO above $14.00 per share.

The final name on the list is Hecla Mining, one of the world's larger silver producers, which is on track to produce 42 million silver-equivalent ounces this year. Notably, the company's costs are well below the industry average and are expected to come in at $10.00/oz after by-product credits, translating to nearly 60% margins. This makes Hecla a rare breed in the silver space, given that most of its peers have costs above $12.00/oz and have a significant chunk of their production in South America or Mexico. In Hecla's case, its operations are in low-risk jurisdictions like Alaska, Nevada, and Idaho.

(Source: TC2000.com)

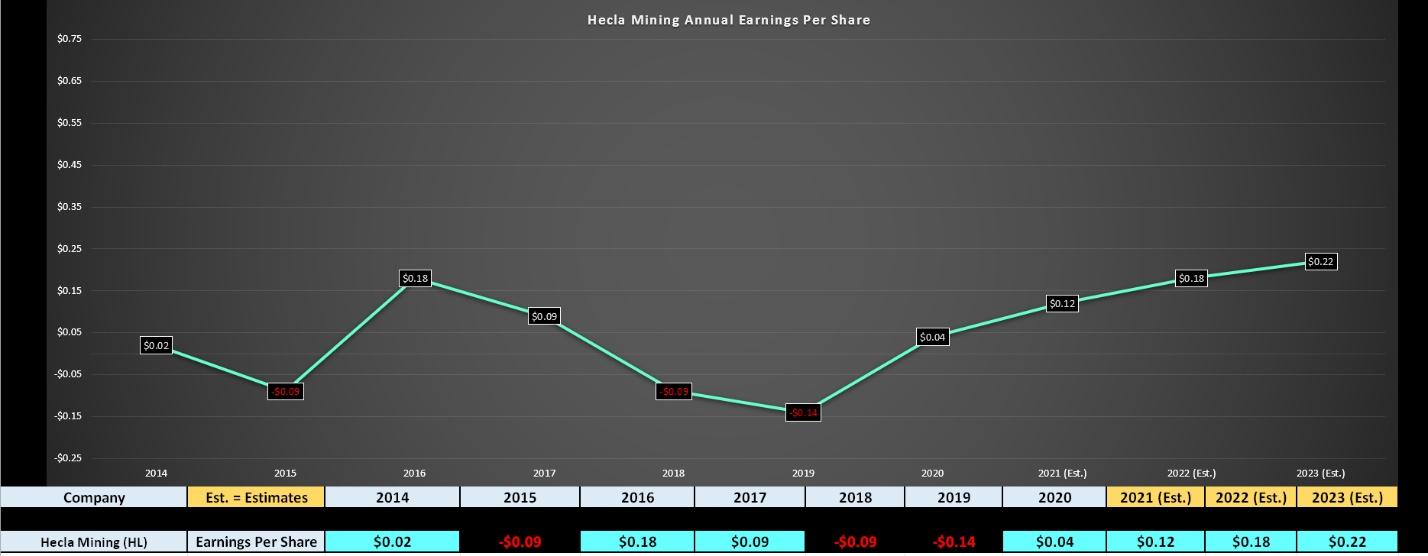

Unfortunately, while the company had a decent year, it saw higher turnover at its flagship Greens Creek Mine in Q3, leading to a slight miss on the Q3 results. Combined with a weaker silver price in H2, earnings estimates have slid to $0.12, down from $0.18 previously for FY2021. Given the large miss in a weak period for the miners, HL has now found itself nearly 45% from its highs above $8.50 per share.

(Source: TC2000.com)

With Hecla trading at more than 20x FY2023 earnings estimates, there are several better value plays out there in the gold space, including Agnico Eagle Mines. However, one thing that HL does have going for it is that it's extremely oversold currently, trading in the lower portion of its multi-year range. As the chart above shows, a move just to the mid-point would represent almost 30% upside, and HL has typically overshot the mid-point after hitting the bottom of its range. So, from a swing-trading standpoint, the stock would become very attractive if it filled its gap at $4.85.

The precious metals stocks continue to be hated, but with most of them heading into the new year oversold and at very attractive valuations, I believe some exposure to the sector makes sense. While AEM is my favored way to play the sector, EGO, GOLD, and HL also look like interesting ideas, with low-risk buy points at $8.80, $18.50, and $4.85 respectively. So, while I think the safest way to play the sector is with AEM or AGI, I believe HL, EGO, and GOLD are three stocks to keep a close eye on if we see further weakness in the sector.

Disclosure: I am long GLD, AEM

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Given the volatility in the precious metals sector, position sizing is critical, so when buying precious metals stocks, position sizes should be limited to 5% or less of one's portfolio.

GLD shares were trading at $168.71 per share on Monday morning, down $2.25 (-1.32%). Year-to-date, GLD has declined -5.41%, versus a 28.97% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles.

The post 3 Gold and Silver Miners With Bright Prospects in 2022 appeared first on StockNews.com