If you are wondering why Home Depot (NYSE: HD) results were no catalyst for the bulls it’s because the news just kicked the risk down the road. The revenue and earnings were better than expected but, after taking the guidance into account, the Q4 period may be on the weak side and the outlook for contraction is still there. The rise of inflation and interest rates is having an impact on sales and that impact is getting worse while inventory grows on a YOY basis. The takeaway is that institutions were selling this stock before the Q3 results were released and there is no reason to think they’re going to start rushing into the name now. The more likely scenario is that they’ll rotate into competitor Lowe’s (NYSE: LOW) because it is better positioned for the times with a higher DIY mix and lower exposure to commercial channels.

The Institutions Keep Home Depot Range Bound

The institutional activity is keeping Home Depot range-bound and that is likely to continue in the near to short-term at least. There was a little bit of buying on a net basis in early calendar Q4 2022 but that trend could easily change given the activity of the prior 2 quarters. The institutions were net sellers in both of those quarters, an activity that drove share prices into the range and then kept them there, and the selling was on the heavier side. In total, net activity for the calendar Q2 and Q3 periods was bearish in the amount of $4.38 billion or about 1.4% of the company. That may sound like a small amount but it is enough of a headwind to keep shares from moving higher within the void of truly good news.

The Q3 results were good, no doubt about it, but the outlook remains unchanged. The company beat top and bottom-line results by wide margins but kept the full-year 2022 guidance unchanged which means the strength is priced into the market if early in coming. The $38.78 billion in revenue is up 5.6% versus last year and beat by $0.910 or 240 basis points which is good, but the gains are driven by an increase in prices that was offset by volume. On a comp basis, sales are up 4.3% systemwide and 4.5% in the US which is above expectations as well and there is strength on the bottom line as well. The $4.24 in GAAP EPS is up 8% YOY on a very slim improvement in operating margin and aided by a 2.8% reduction in share count.

Turning to the guidance, the only reaffirmed the Q4 guidance despite the obvious strength in Q3 results. The company is expecting revenue growth of 3% which is well below the analyst's estimates and there are other problems to worry about as well. The company reports inventory is down on a sequential basis but only by a small 150 basis points compared to the 1150 basis points expected by the market. The inventory is up 25% however, on a YOY basis, and will continue to weigh on profitability (and the broader market) going forward. The real risk is that some items will have to go on markdown or worse, clearance or back into storage, and that will have a negative impact on profitability.

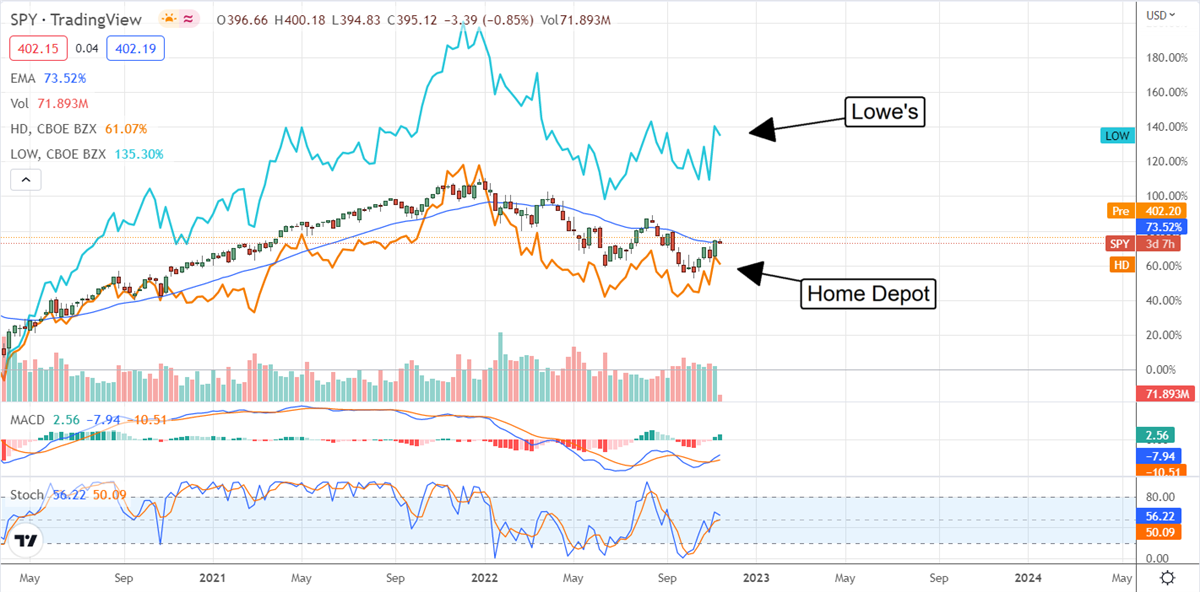

Home Depot Or Lowe’s, Value And Dividends Matter

Home Depot pays a healthy 2.5% and it is a growing distribution but there is risk compared to Lowe’s that may sway investors. The company has only been raising its dividend for about 12 years because it did not pay a distribution during the Great Recession. Lowe’s, on the other hand, is a Dividend Aristocrat and a Dividend King with more than 59 years of consecutive annual increases. With a housing-led recession about to unfold, it is clear which dividend is more trustworthy and Lowe’s comes with a lower valuation, 15X compared to 18, and a better outlook for distribution growth.

The charts may also help sway the market into its decision, Lowe’s or Home Depot because Lowe’s is clearly the outperformer in the post-pandemic world. Home Depot is underperforming the broad market, actually, while Lowe’s outperforms by triple-digits even with the headwind of institutional selling. If that changes, Lowe’s could easily see its share prices accelerate.