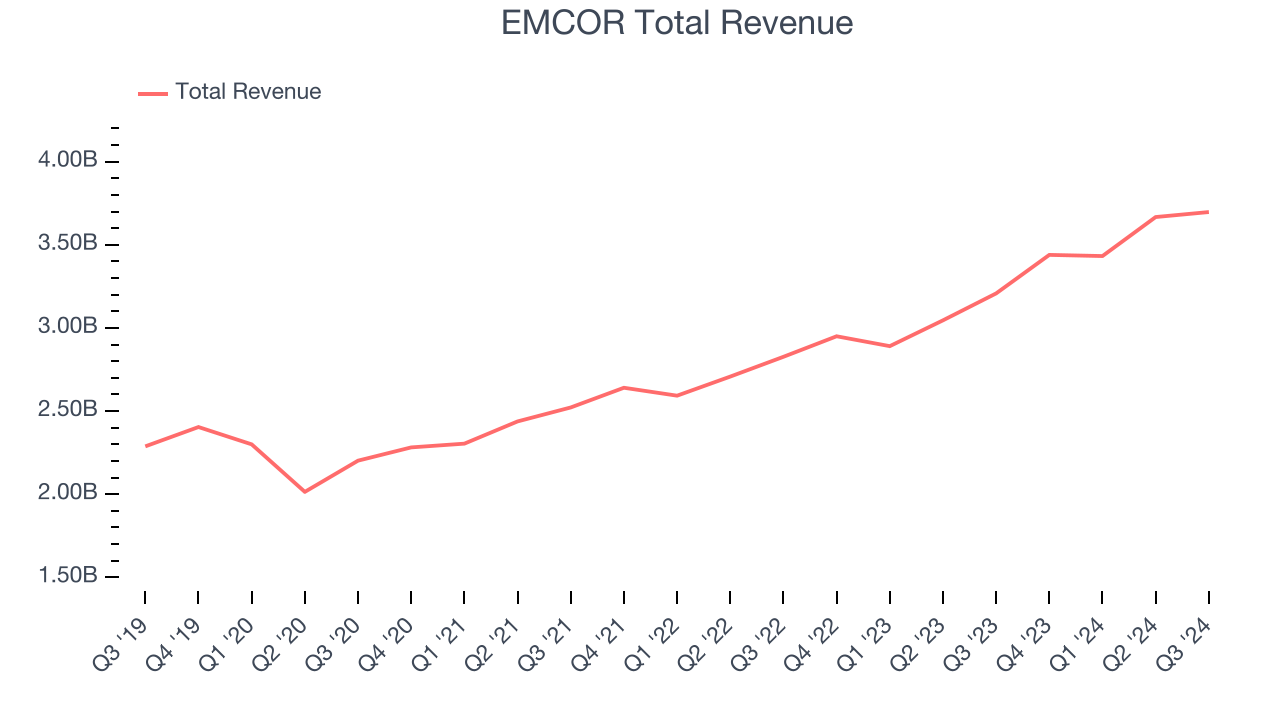

Specialty construction contractor company EMCOR (NYSE:EME) missed Wall Street’s revenue expectations in Q3 CY2024, but sales rose 15.3% year on year to $3.70 billion. The company’s full-year revenue guidance of $14.5 billion at the midpoint also came in 1.7% below analysts’ estimates. Its non-GAAP profit of $5.80 per share was 16.8% above analysts’ consensus estimates.

Is now the time to buy EMCOR? Find out by accessing our full research report, it’s free.

EMCOR (EME) Q3 CY2024 Highlights:

- Revenue: $3.70 billion vs analyst estimates of $3.79 billion (2.5% miss)

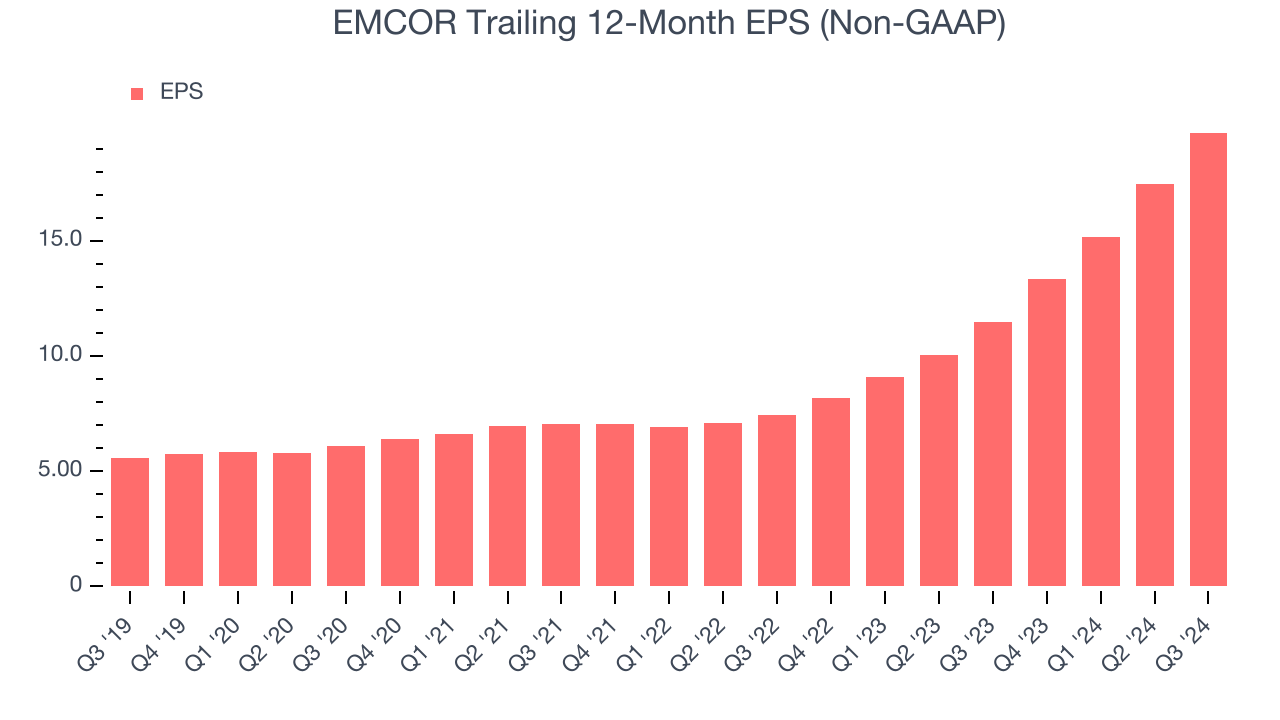

- Adjusted EPS: $5.80 vs analyst estimates of $4.97 (16.8% beat)

- EBITDA: $408.9 million vs analyst estimates of $351 million (16.5% beat)

- The company dropped its revenue guidance for the full year to $14.5 billion at the midpoint from $14.75 billion, a 1.7% decrease

- Adjusted EPS guidance for the full year is $20.75 at the midpoint, beating analyst estimates by 6.1%

- Gross Margin (GAAP): 19.9%, up from 17% in the same quarter last year

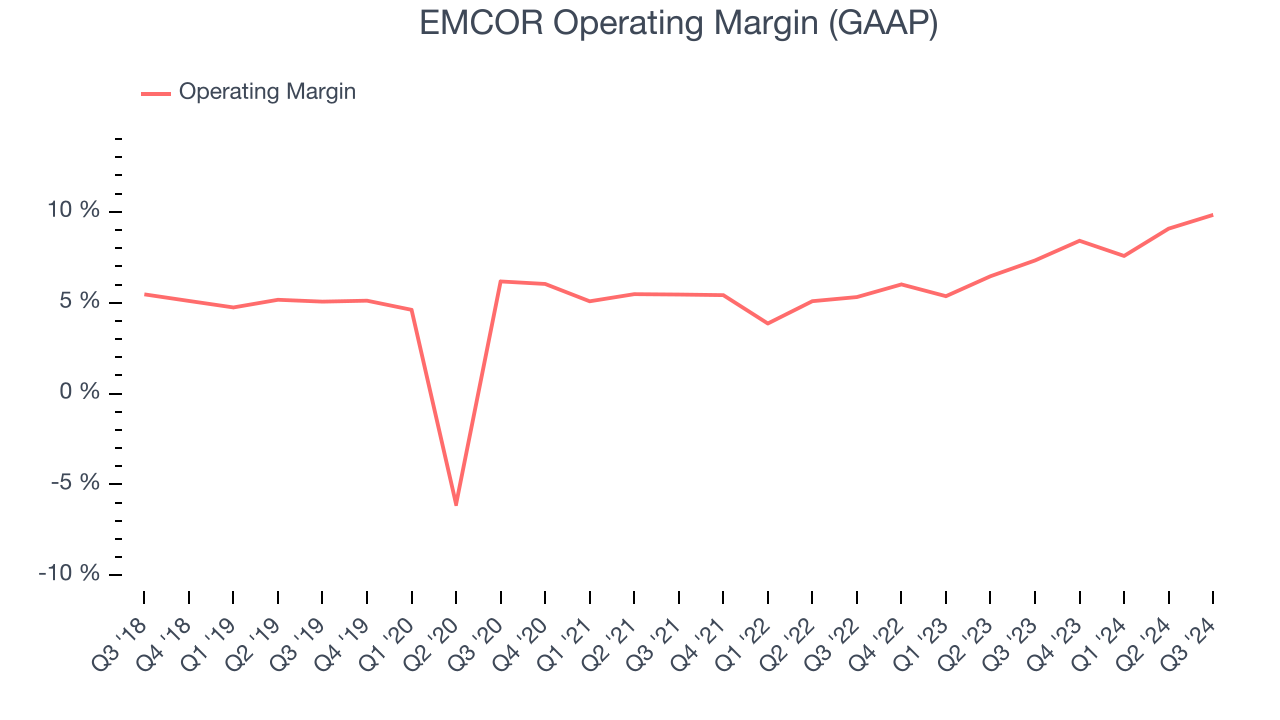

- Operating Margin: 9.8%, up from 7.3% in the same quarter last year

- EBITDA Margin: 11.1%, up from 8.3% in the same quarter last year

- Free Cash Flow Margin: 13.8%, up from 7.5% in the same quarter last year

- Market Capitalization: $20.15 billion

Tony Guzzi, Chairman, President, and Chief Executive Officer of EMCOR, commented, “Our team continued to perform exceptionally well and delivered another great quarter, maintaining our momentum and again setting new records across key financial and operational metrics. Record RPOs of $9.8 billion, along with a robust and diverse pipeline of future opportunities, demonstrates the continued demand for our services. Our record operating cash flow and strong and liquid balance sheet enable us to compete and win on sophisticated projects, and support our organic growth and balanced capital allocation strategy.”

Company Overview

Through its network of over 70 subsidiaries, EMCOR (NYSE:EME) provides electrical, mechanical, and building construction and services

Engineering and Design Services

Companies providing engineering and design services boast ever-evolving technical expertise. Compared to their counterparts who manufacture and sell physical products, these companies can also pivot faster to more trending areas due to their smaller physical asset bases. Green energy and water conservation, for example, are current themes driving incremental demand in this space. On the other hand, those providing engineering and design services are at the whim of construction and infrastructure project volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates.

Sales Growth

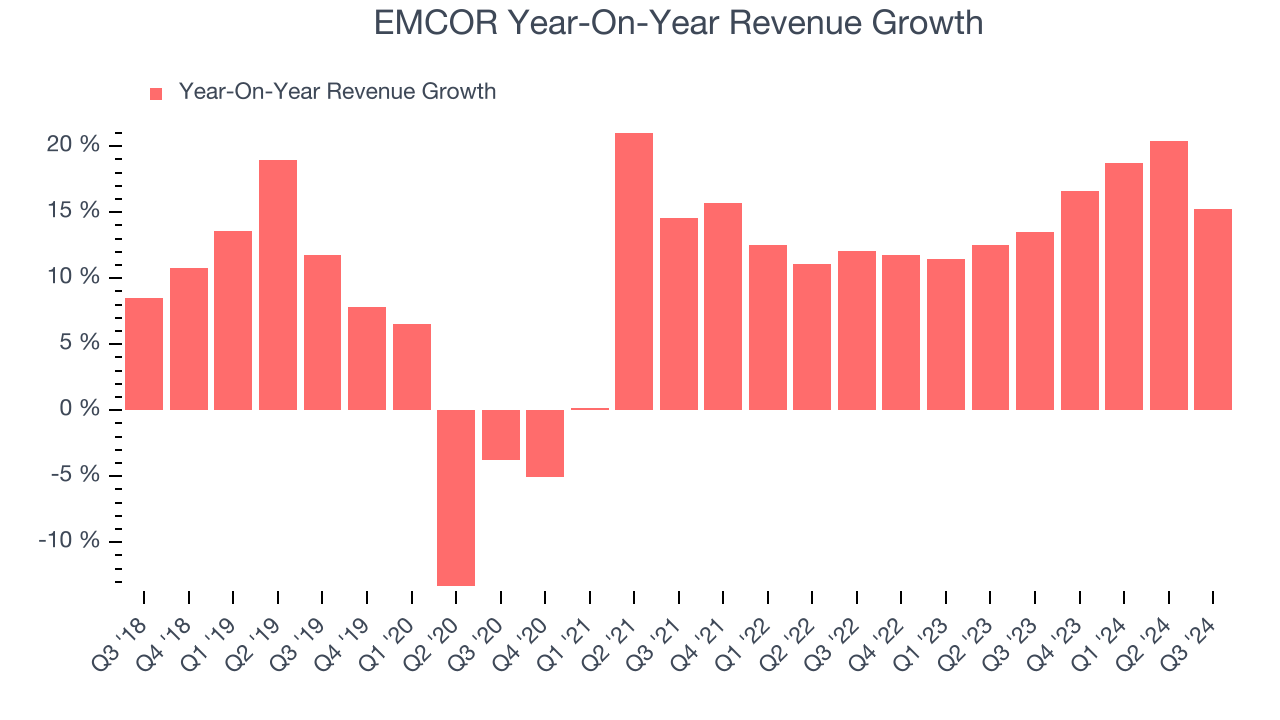

Examining a company’s long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, EMCOR’s sales grew at a solid 9.6% compounded annual growth rate over the last five years. This is encouraging because it shows EMCOR was more successful in expanding than most industrials companies.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. EMCOR’s annualized revenue growth of 15% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

We can dig further into the company’s revenue dynamics by analyzing its most important segments, Mechanical Construction and Facilities Services and Building Services , which are 45% and 21.6% of revenue. Over the last two years, EMCOR’s Mechanical Construction and Facilities Services revenue (design, integration, installation) averaged 21.7% year-on-year growth while its Building Services revenue (maintenance, electrical, plumbing) averaged 9.3% growth.

This quarter, EMCOR’s revenue grew 15.3% year on year to $3.70 billion, falling short of Wall Street’s estimates.

We also like to judge companies based on their projected revenue growth, but not enough Wall Street analysts cover the company for it to have reliable consensus estimates. This signals EMCOR could be a hidden gem because it doesn’t get attention from professional brokers.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Operating Margin

EMCOR was profitable over the last five years but held back by its large cost base. Its average operating margin of 6% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

On the plus side, EMCOR’s annual operating margin rose by 6 percentage points over the last five years, as its sales growth gave it immense operating leverage.

In Q3, EMCOR generated an operating profit margin of 9.8%, up 2.5 percentage points year on year. Since its gross margin expanded more than its operating margin, we can infer that leverage on its cost of sales was the primary driver behind the recently higher efficiency.

Earnings Per Share

Analyzing revenue trends tells us about a company’s historical growth, but the long-term change in its earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

EMCOR’s EPS grew at an astounding 28.7% compounded annual growth rate over the last five years, higher than its 9.6% annualized revenue growth. This tells us the company became more profitable as it expanded.

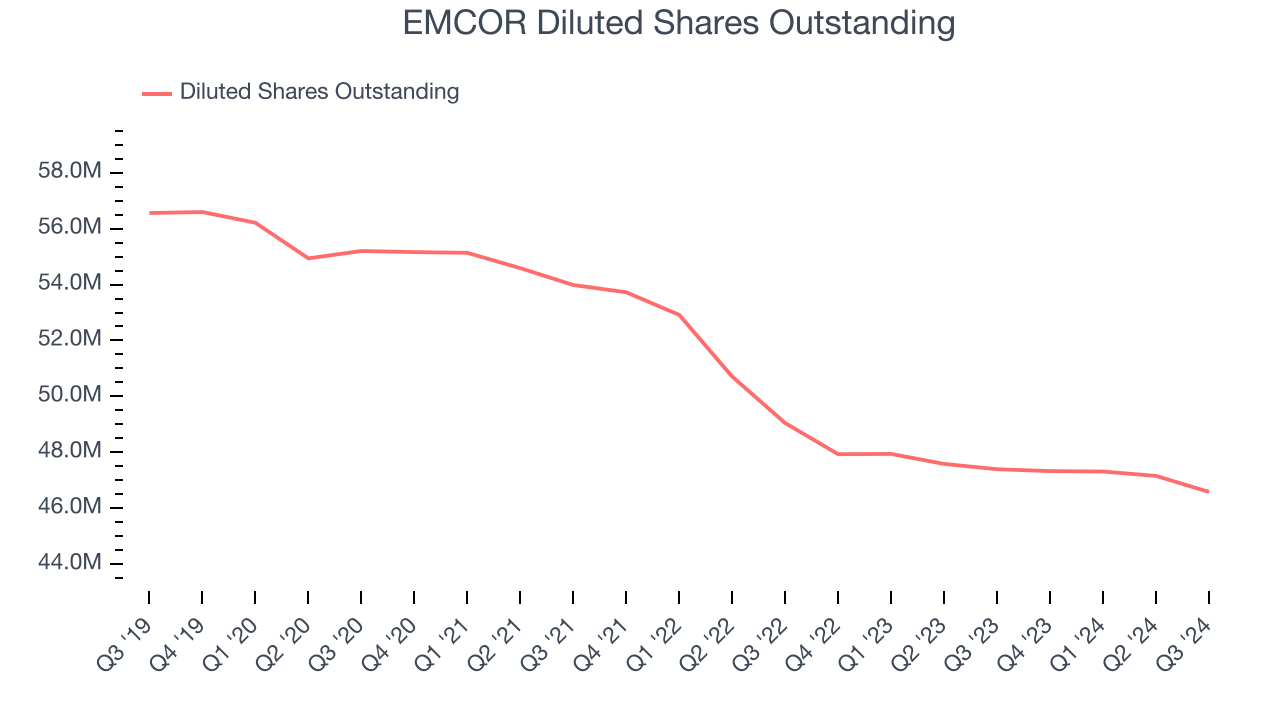

Diving into EMCOR’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, EMCOR’s operating margin expanded by 6 percentage points over the last five years. On top of that, its share count shrank by 17.6%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For EMCOR, its two-year annual EPS growth of 62.9% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.In Q3, EMCOR reported EPS at $5.80, up from $3.59 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data. This signals EMCOR could be a hidden gem because it doesn’t have much coverage among professional brokers.

Key Takeaways from EMCOR’s Q3 Results

This quarter, EMCOR beat on profitability but missed on revenue - its EBITDA and EPS topped expectations while its revenue missed due to underperformance in its Mechanical Construction and Facilities Services segment. Its full-year EPS guidance also beat analysts' estimates while its revenue outlook fell short. Overall, this was a mixed quarter. The market seemed to care more about the better-than-anticipated profitability, and the stock traded up 5.1% to $453.35 immediately after reporting.

Is EMCOR an attractive investment opportunity right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.