Wrapping up Q3 earnings, we look at the numbers and key takeaways for the construction and engineering stocks, including MDU Resources (NYSE:MDU) and its peers.

Construction and engineering companies not only boast technical know-how in specialized areas but also may hold special licenses and permits. Those who work in more regulated areas can enjoy more predictable revenue streams - for example, sprinkler systems need to be maintained every three years. More recently, services addressing energy efficiency and labor availability are also creating incremental demand. But like the broader industrials sector, construction and engineering companies are at the whim of economic cycles as external factors like interest rates can greatly impact the new construction that drives topline performance for these companies.

The 20 construction and engineering stocks we track reported a mixed Q3. As a group, revenues missed analysts’ consensus estimates by 1.2% while next quarter’s revenue guidance was 1.9% below.

Luckily, construction and engineering stocks have performed well with share prices up 14.5% on average since the latest earnings results.

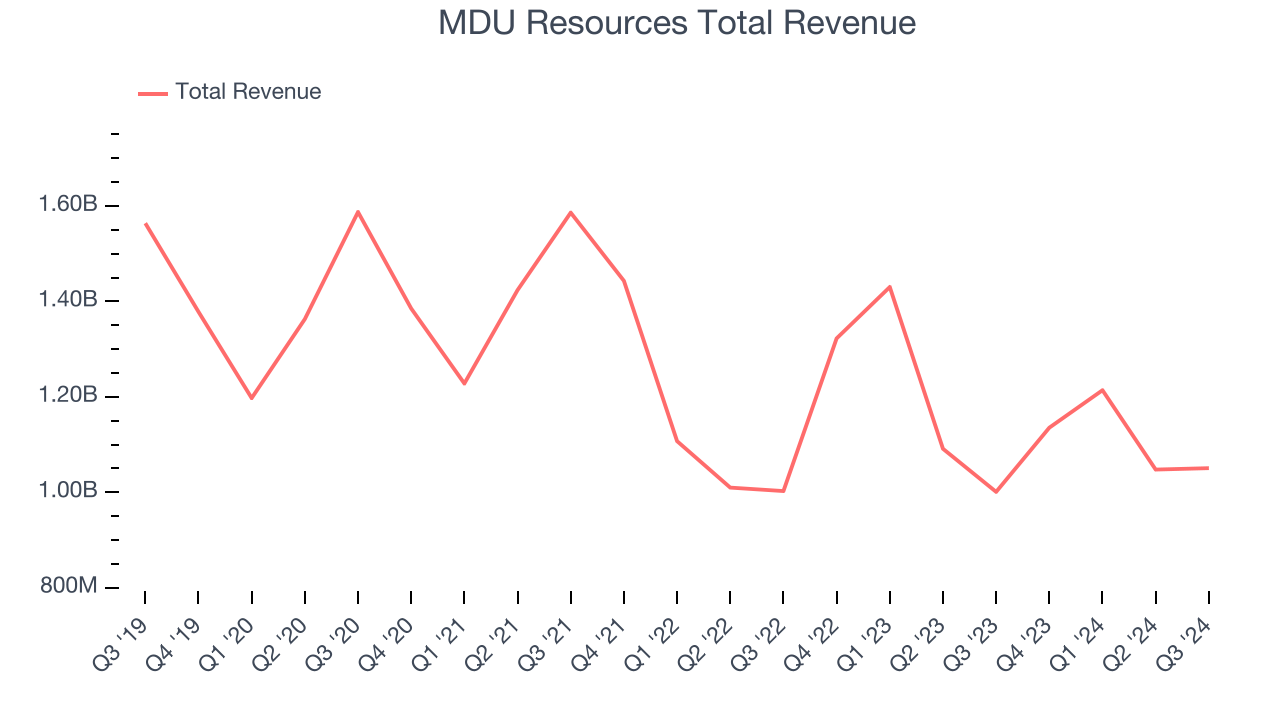

MDU Resources (NYSE:MDU)

Founded to provide electricity to towns in Minnesota, MDU Resources (NYSE:MDU) provides products and services in the utilities and construction materials industries.

MDU Resources reported revenues of $1.05 billion, up 5% year on year. This print exceeded analysts’ expectations by 4.9%. Overall, it was a strong quarter for the company with a solid beat of analysts’ EPS estimates.

"The successful spinoff of Everus Construction Group on October 31, following last year's Knife River Corporation spinoff, marks the completion of our strategic initiatives," said Nicole A. Kivisto, president and CEO of MDU Resources.

MDU Resources scored the biggest analyst estimates beat of the whole group. Unsurprisingly, the stock is up 19.1% since reporting and currently trades at $20.18.

Is now the time to buy MDU Resources? Access our full analysis of the earnings results here, it’s free.

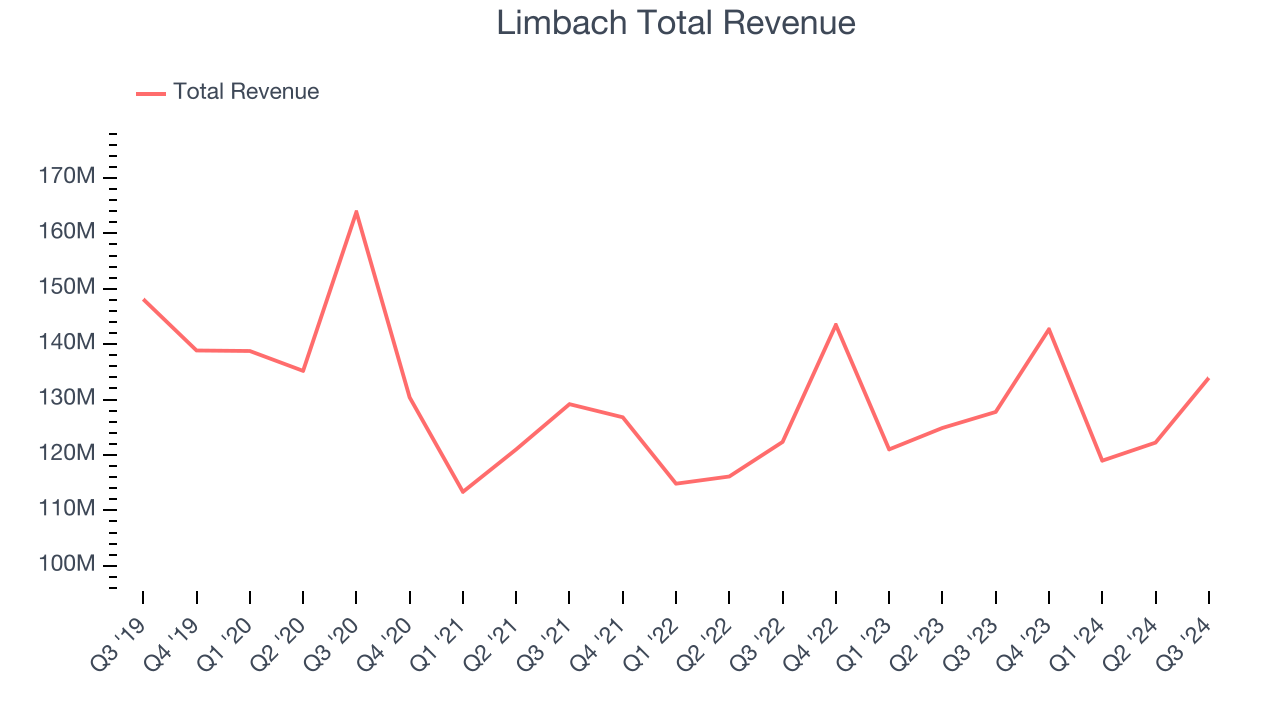

Best Q3: Limbach (NASDAQ:LMB)

Established in 1901, Limbach (NASDAQ: LMB) provides integrated building systems solutions, including mechanical, electrical, and plumbing services.

Limbach reported revenues of $133.9 million, up 4.8% year on year, outperforming analysts’ expectations by 3.4%. The business had a stunning quarter with an impressive beat of analysts’ EPS estimates and an impressive beat of analysts’ EBITDA estimates.

Limbach pulled off the highest full-year guidance raise among its peers. The market seems happy with the results as the stock is up 31.9% since reporting. It currently trades at $102.88.

Is now the time to buy Limbach? Access our full analysis of the earnings results here, it’s free.

Slowest Q3: Tutor Perini (NYSE:TPC)

Known for constructing the Philadelphia Eagles’ Stadium, Tutor Perini (NYSE:TPC) is a civil and building construction company offering diversified general contracting and design-build services.

Tutor Perini reported revenues of $1.08 billion, up 2.1% year on year, falling short of analysts’ expectations by 7.2%. It was a disappointing quarter as it posted a significant miss of analysts’ EPS estimates.

As expected, the stock is down 5.6% since the results and currently trades at $28.57.

Read our full analysis of Tutor Perini’s results here.

Ameresco (NYSE:AMRC)

Having played a role in upgrading the energy solutions of Alcatraz Island, Ameresco (NYSE:AMRC) provides energy and renewable energy solutions for various sectors.

Ameresco reported revenues of $500.9 million, up 49.4% year on year. This number topped analysts’ expectations by 3%. More broadly, it was a slower quarter as it recorded a significant miss of analysts’ adjusted operating income estimates and a significant miss of analysts’ EBITDA estimates.

The stock is down 11.5% since reporting and currently trades at $28.

Read our full, actionable report on Ameresco here, it’s free.

FTAI Infrastructure (NASDAQ:FIP)

Spun off from FTAI Aviation in 2021, FTAI Infrastructure (NASDAQ:FIP) invests in and operates infrastructure and related assets across the transportation and energy sectors.

FTAI Infrastructure reported revenues of $83.31 million, up 3.2% year on year. This print lagged analysts' expectations by 11.7%. Overall, it was a disappointing quarter as it also produced a significant miss of analysts’ EPS estimates and a miss of analysts’ EBITDA estimates.

FTAI Infrastructure had the weakest performance against analyst estimates among its peers. The stock is up 4.9% since reporting and currently trades at $8.96.

Read our full, actionable report on FTAI Infrastructure here, it’s free.

Market Update

Thanks to the Fed's series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market has thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% in November), and a notable surge followed Donald Trump’s presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by potential trade policy changes and corporate tax discussions, which could impact business confidence and growth. The path forward holds both optimism and caution as new policies take shape.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.