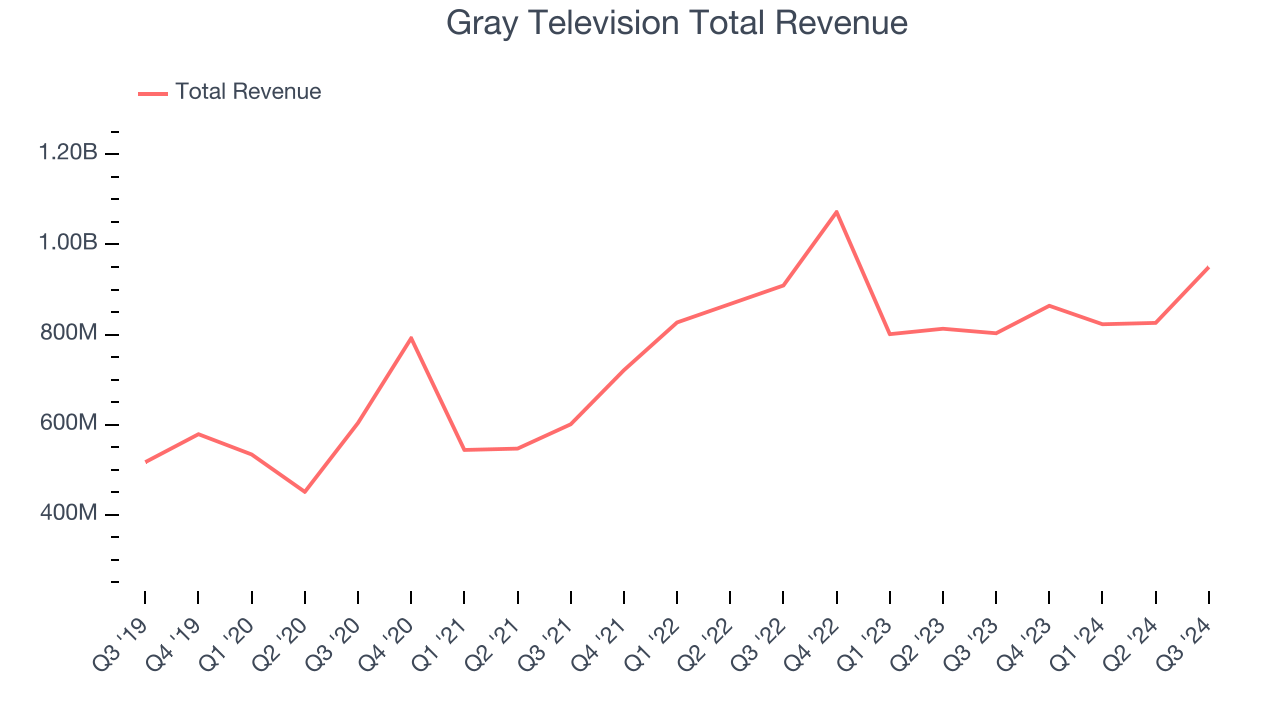

Local television broadcasting and media company Gray Television (NYSE:GTN) missed Wall Street’s revenue expectations in Q3 CY2024, but sales rose 18.3% year on year to $950 million. Next quarter’s revenue guidance of $943 million underwhelmed, coming in 20.7% below analysts’ estimates. Its GAAP profit of $0.86 per share was also 5.8% below analysts’ consensus estimates.

Is now the time to buy Gray Television? Find out by accessing our full research report, it’s free.

Gray Television (GTN) Q3 CY2024 Highlights:

- Revenue: $950 million vs analyst estimates of $967.6 million (1.8% miss)

- EPS: $0.86 vs analyst expectations of $0.91 (5.8% miss)

- EBITDA: $338 million vs analyst estimates of $342 million (1.2% miss)

- Revenue Guidance for Q4 CY2024 is $943 million at the midpoint, below analyst estimates of $1.19 billion

- Gross Margin (GAAP): 37.6%, up from 28.4% in the same quarter last year

- Operating Margin: 26.3%, up from 10.5% in the same quarter last year

- EBITDA Margin: 35.6%, up from 25.5% in the same quarter last year

- Market Capitalization: $565.1 million

Company Overview

Specializing in local media coverage, Gray Television (NYSE:GTN) is a broadcast company supplying digital media to various markets in the United States.

Broadcasting

Broadcasting companies have been facing secular headwinds in the form of consumers abandoning traditional television and radio in favor of streaming services. As a result, many broadcasting companies have evolved by forming distribution agreements with major streaming platforms so they can get in on part of the action, but will these subscription revenues be as high quality and high margin as their legacy revenues? Only time will tell which of these broadcasters will survive the sea changes of technological advancement and fragmenting consumer attention.

Sales Growth

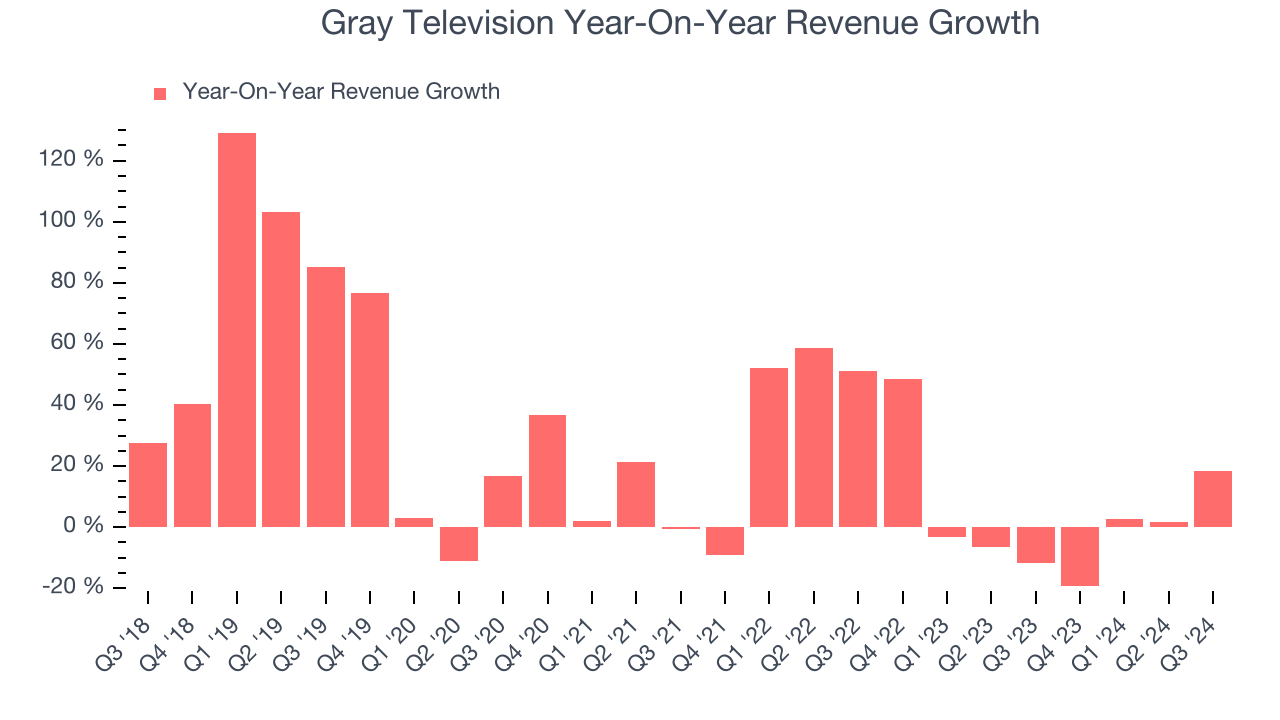

A company’s long-term performance can indicate its business quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Gray Television grew its sales at a mediocre 13.1% compounded annual growth rate. This shows it couldn’t expand in any major way, a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or emerging trend. Gray Television’s recent history shows its demand slowed as its annualized revenue growth of 2.1% over the last two years is below its five-year trend.

We can dig further into the company’s revenue dynamics by analyzing its most important segments, Retransmission and Advertising, which are 38.8% and 38.4% of revenue. Over the last two years, Gray Television’s Retransmission revenue (affiliate and licensing fees) averaged 2.3% year-on-year growth while its Advertising revenue (marketing services) averaged 2.6% growth.

This quarter, Gray Television’s revenue grew 18.3% year on year to $950 million, falling short of Wall Street’s estimates. Management is currently guiding for a 9.1% year-on-year increase next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 3% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and illustrates the market thinks its newer products and services will not catalyze better top-line performance yet.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Cash Is King

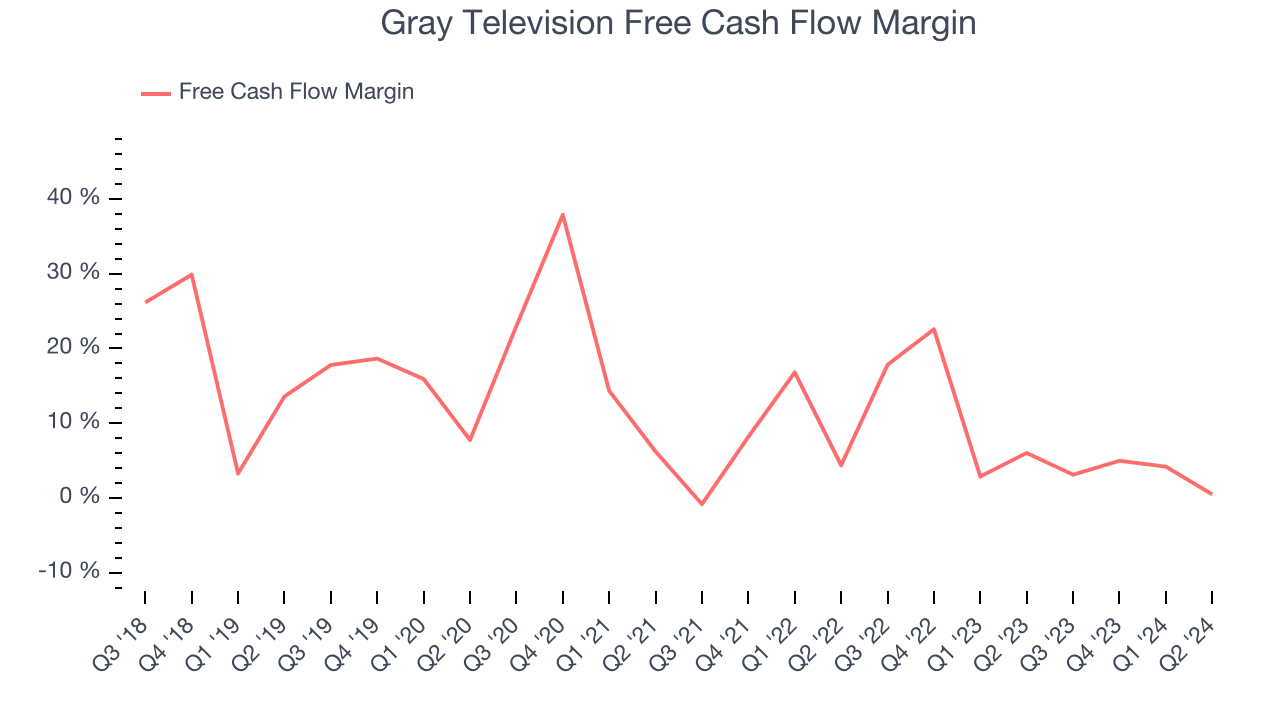

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Gray Television has shown weak cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 7%, subpar for a consumer discretionary business. The divergence from its good operating margin stems from its capital-intensive business model, which requires Gray Television to make large cash investments in working capital and capital expenditures.

Key Takeaways from Gray Television’s Q3 Results

We struggled to find many strong positives in these results as its revenue, EPS, and EBITDA missed Wall Street's estimates. Its full-year revenue guidance also fell short. Overall, this was a softer quarter, but the stock traded up 1% to $5.85 immediately after reporting - likely because buy-side expectations were even lower than published sell-side projections.

So should you invest in Gray Television right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.