Wendy's currently trades at $17.26 per share and has shown little upside over the past six months, posting a middling return of 2.4%. The stock also fell short of the S&P 500’s 11.9% gain during that period.

Is now the time to buy Wendy's, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.We're sitting this one out for now. Here are three reasons why you should be careful with WEN and a stock we'd rather own.

Why Is Wendy's Not Exciting?

Founded by Dave Thomas in 1969, Wendy’s (NASDAQ:WEN) is a renowned fast-food chain known for its fresh, never-frozen beef burgers, flavorful menu options, and commitment to quality.

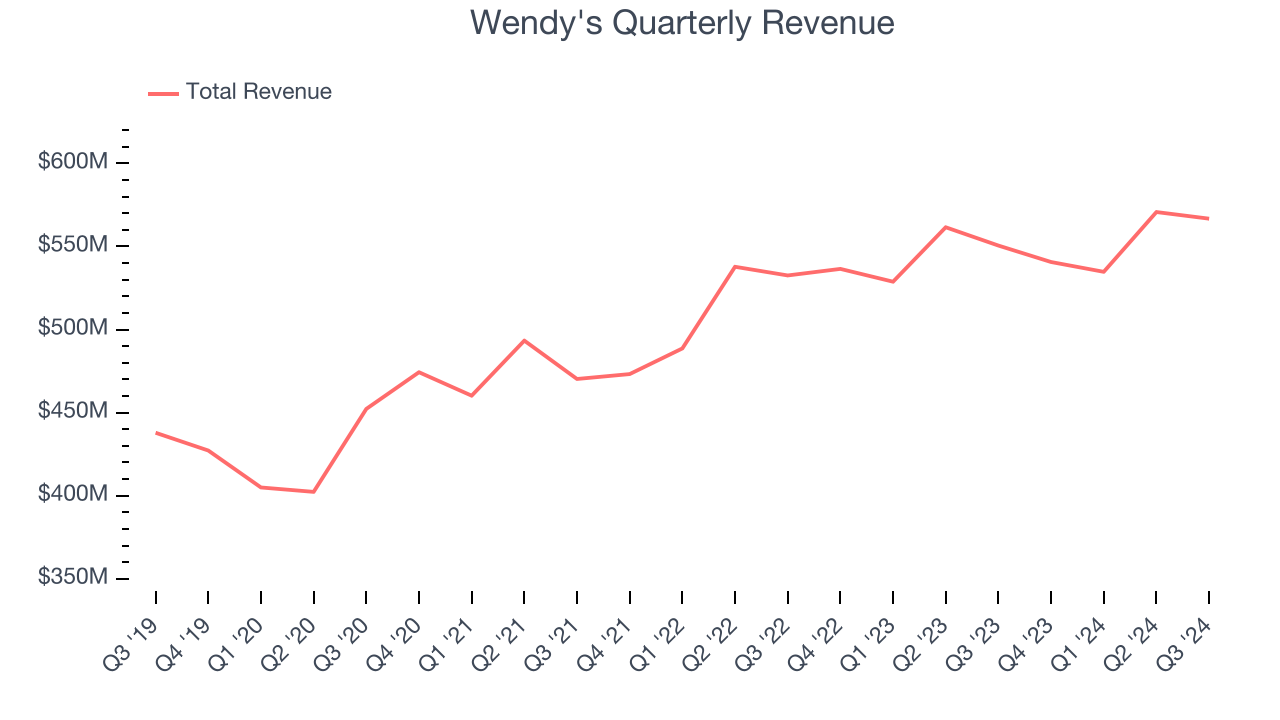

1. Long-Term Revenue Growth Disappoints

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years. Over the last five years, Wendy's grew its sales at a tepid 5.7% compounded annual growth rate. This fell short of our benchmark for the restaurant sector.

2. Operating Margin Falling

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Looking at the trend in its profitability, Wendy’s operating margin decreased by 1.1 percentage points over the last year. Even though its historical margin is high, shareholders will want to see Wendy's become more profitable in the future. Its operating margin for the trailing 12 months was 16.4%.

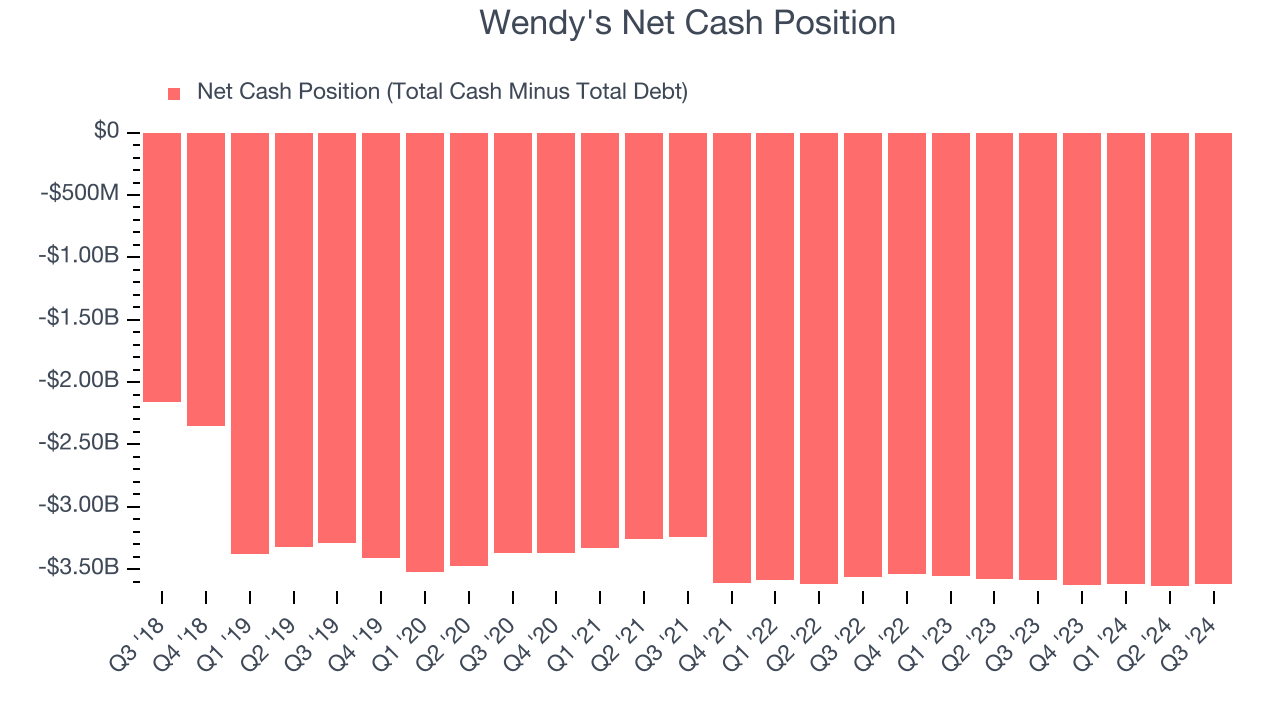

3. High Debt Levels Increase Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Wendy’s $4.10 billion of debt exceeds the $482.2 million of cash on its balance sheet. Furthermore, its 7× net-debt-to-EBITDA ratio (based on its EBITDA of $532.7 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Wendy's could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Wendy's can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

Final Judgment

Wendy's isn’t a terrible business, but it doesn’t pass our quality test. With its shares lagging the market recently, the stock trades at 6.4× forward EV-to-EBITDA (or $17.26 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're fairly confident there are better stocks to buy right now. We’d suggest looking at FTAI Aviation, an aerospace company benefiting from Boeing and Airbus’s struggles.

Stocks We Would Buy Instead of Wendy's

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.