What a fantastic six months it’s been for TEGNA. Shares of the company have skyrocketed 45.4%, hitting $18.50. This run-up might have investors contemplating their next move.

Is now the time to buy TEGNA, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.Despite the momentum, we don't have much confidence in TEGNA. Here are three reasons why there are better opportunities than TGNA and a stock we'd rather own.

Why Is TEGNA Not Exciting?

Spun out of Gannett in 2015, TEGNA (NYSE:TGNA) is a media company operating a network of television stations and digital platforms, focusing on local news and community content.

1. Long-Term Revenue Growth Disappoints

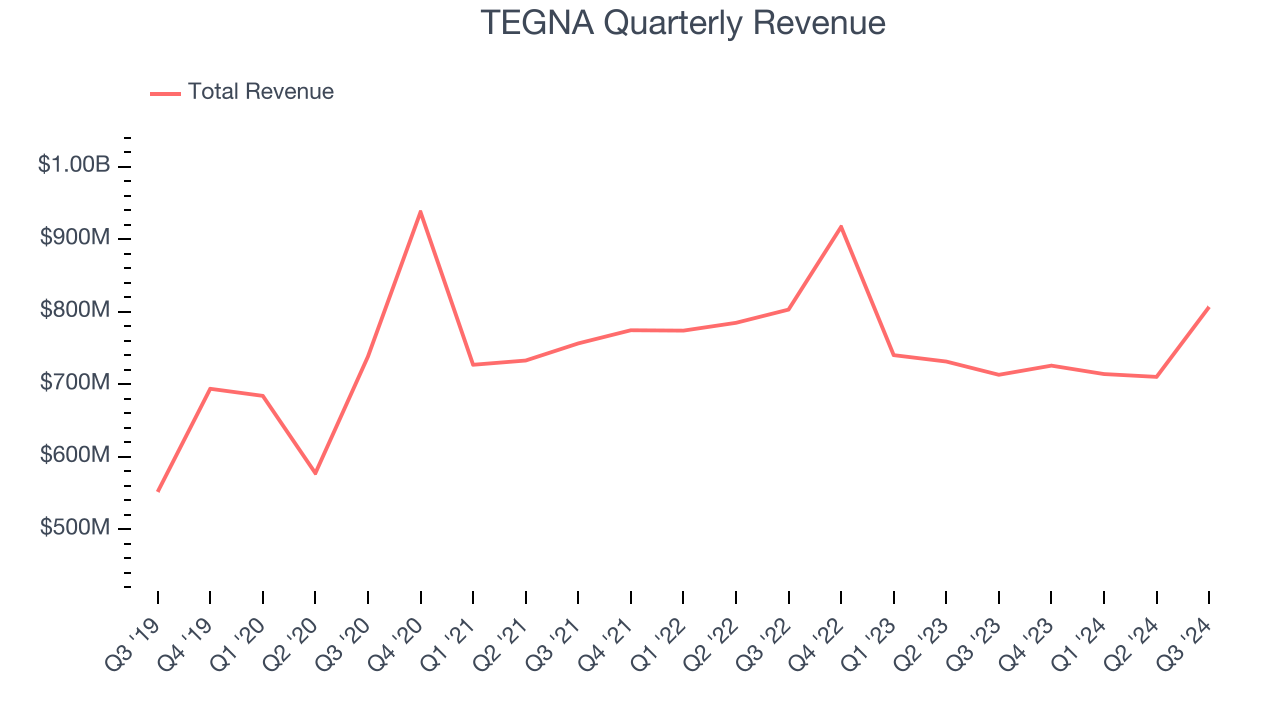

A company’s long-term sales performance signals its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, TEGNA’s sales grew at a sluggish 5.6% compounded annual growth rate over the last five years. This was below our standard for the consumer discretionary sector.

2. Cash Flow Margin Set to Decline

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Over the next year, analysts predict TEGNA’s cash conversion will fall. Their consensus estimates imply its free cash flow margin of 18.7% for the last 12 months will decrease to 15.3%.

3. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect TEGNA’s revenue to rise by 2.4%. While this projection suggests its newer products and services will fuel better top-line performance, it is still below the sector average.

Final Judgment

TEGNA isn’t a terrible business, but it isn’t one of our picks. After the recent rally, the stock trades at 6.2× forward price-to-earnings (or $18.50 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at KLA Corporation, a picks and shovels play for semiconductor manufacturing.

Stocks We Would Buy Instead of TEGNA

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.