Spectrum Brands has been treading water for the past six months, recording a small loss of 3.2% while holding steady at $85.43. The stock also fell short of the S&P 500’s 9.2% gain during that period.

Is there a buying opportunity in Spectrum Brands, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.We're sitting this one out for now. Here are three reasons why you should be careful with SPB and a stock we'd rather own.

Why Do We Think Spectrum Brands Will Underperform?

A leader in multiple consumer product categories, Spectrum Brands (NYSE:SPB) is a diversified company with a portfolio of trusted brands spanning home appliances, garden care, personal care, and pet care.

1. Long-Term Revenue Growth Flatter Than a Pancake

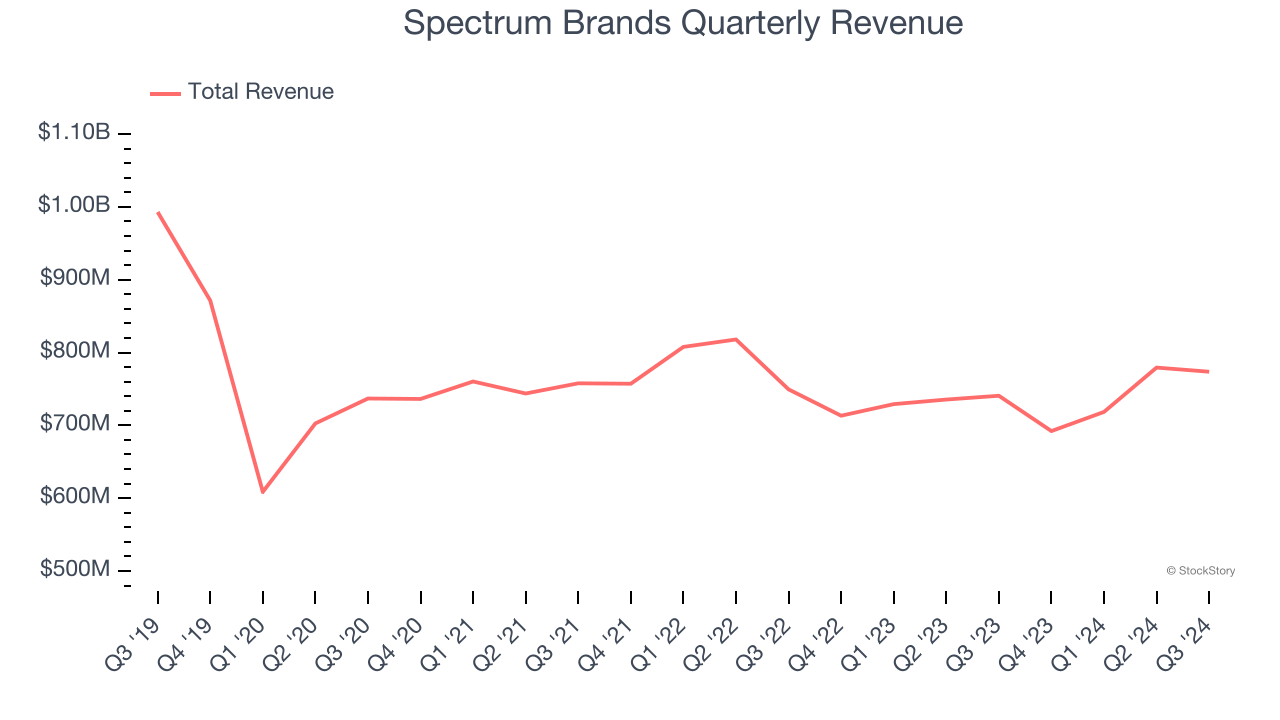

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Spectrum Brands struggled to consistently increase demand as its $2.96 billion of sales for the trailing 12 months was close to its revenue three years ago. This was below our standards and is a sign of poor business quality.

2. Core Business Falling Behind as Demand Declines

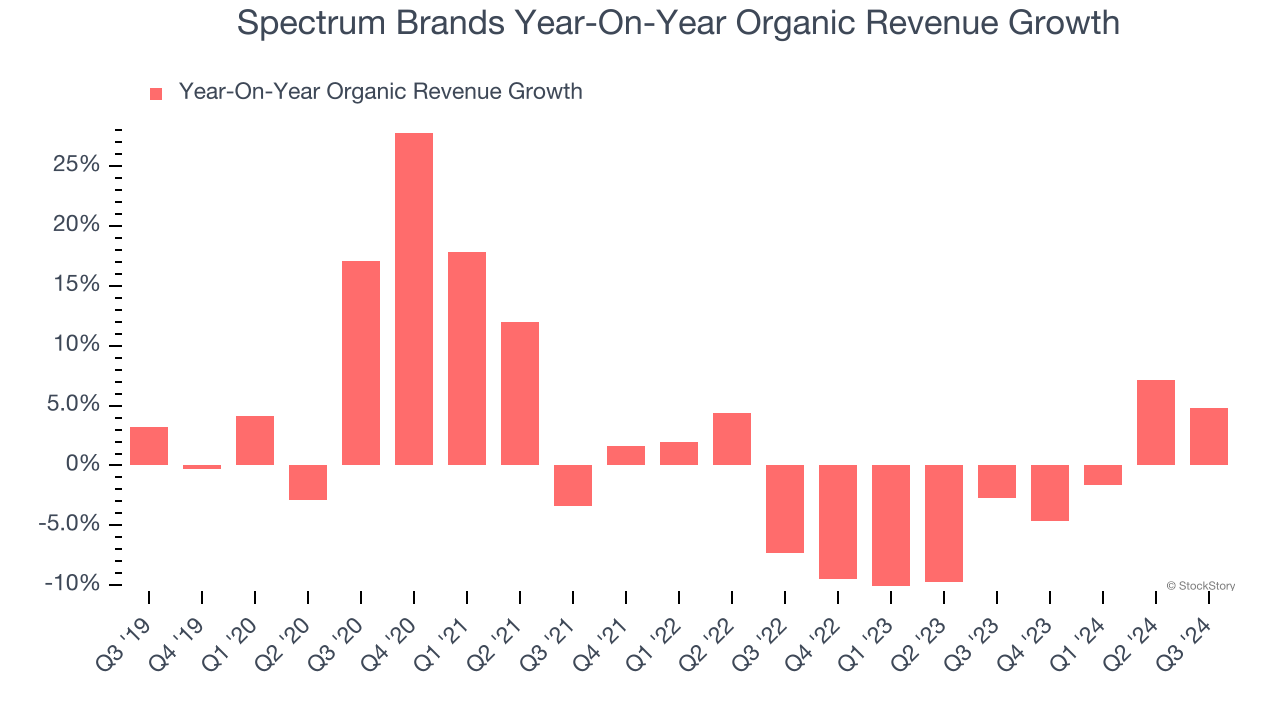

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

Spectrum Brands’s demand has been falling over the last eight quarters, and on average, its organic sales have declined by 3.3% year on year.

3. Cash Burn Ignites Concerns

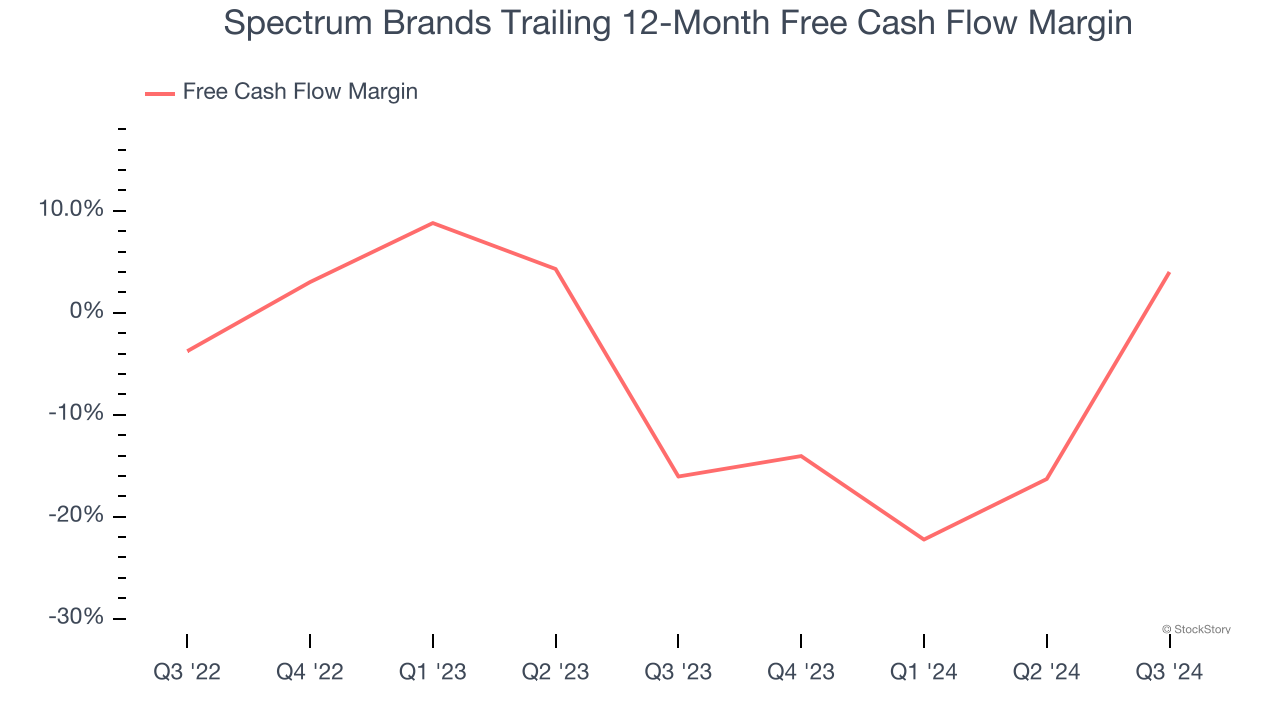

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

While Spectrum Brands posted positive free cash flow this quarter, the broader story hasn’t been so clean. Over the last two years, Spectrum Brands’s demanding reinvestments and muted organic growth have consumed many resources, contributing to an average free cash flow margin of negative 6%. This means it lit $5.95 of cash on fire for every $100 in revenue.

Final Judgment

Spectrum Brands falls short of our quality standards. With its shares lagging the market recently, the stock trades at 15.2× forward price-to-earnings (or $85.43 per share). This valuation multiple is fair, but we don’t have much confidence in the company. There are superior stocks to buy right now. We’d suggest looking at Costco, one of Charlie Munger’s all-time favorite businesses.

Stocks We Like More Than Spectrum Brands

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market to cap off the year - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.